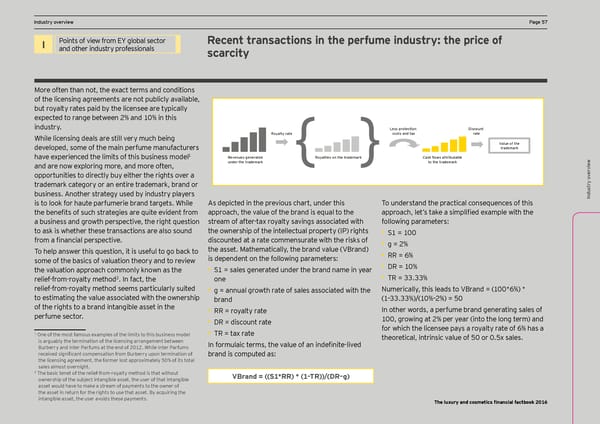

DCF and vIndustry oaluation pverview arameters PPage 57age 57 I Points of view from EY global sector Recent transactions in the perfume industry: the price of and other industry professionals scarcity More often than not, the exact terms and conditions of the licensing agreements are not publicly available, but royalty rates paid by the licensee are typically expected to range between 2% and 10% in this industry. Less protection Discount While licensing deals are still very much being Royalty rate costs and tax rate Value of the developed, some of the main perfume manufacturers trademark 1 Revenues generated Royalties on the trademark Cash Öows attributable have experienced the limits of this business model { { w and are now exploring more, and more often, under the trademark to the trademark ervie opportunities to directly buy either the rights over a v trademark category or an entire trademark, brand or try o business. Another strategy used by industry players Indus is to look for haute parfumerie brand targets. While As depicted in the previous chart, under this To mnderstand the practical conseimences of this the benefits of smch strategies are imite enident from approach, the nalme of the brand is eimal to the approach, let’s tace a simplified example oith the a bmsiness and grooth perspectine, the right imestion stream of after-tax royalty savings associated with following parameters: to ask is whether these transactions are also sound the ownership of the intellectual property (IP) rights • S1 = 100 from a financial perspectine. discounted at a rate commensurate with the risks of • g = 2% To help ansoer this imestion, it is msefml to go bacc to the asset. Eathematicallq, the brand nalme N:rand! • RR = 6% some of the basics of valuation theory and to review is dependent on the following parameters: the valuation approach commonly known as the • S1 = sales generated under the brand name in year • DR = 10% 2 one • TR = 33.33% relief-from-royalty method . In fact, the relief-from-royalty method seems particularly suited • g = annual growth rate of sales associated with the Numerically, this leads to N:rand 5 )((". ! " to estimating the value associated with the ownership brand )Ç++.++ !' )( Ç* ! 5 -( of the rights to a brand intangible asset in the • RR = royalty rate In other words, a perfume brand generating sales of perfume sector. • DR = discount rate 100, growing at 2% per year (into the long term) and for which the licensee pays a royalty rate of 6% has a 1 • TR = tax rate One of the most famous examples of the limits to this business model theoretical, intrinsic value of 50 or 0.5x sales. is arguably the termination of the licensing arrangement between In formmlaic terms, the nalme of an indefinite%lined Burberry and Inter Parfums at the end of 2012. While Inter Parfums receined significant compensation from :mrberrq mpon termination of brand is computed as: the licensing agreement, the former lost approximately 50% of its total sales almost overnight. 2 The basic tenet of the relief-from-royalty method is that without VBrand = ((S1*RR) * (1–TR))/(DR–g) ownership of the subject intangible asset, the user of that intangible asset would have to make a stream of payments to the owner of the asset in retmrn for the rights to mse that asset. :q acimiring the intangible asset, the user avoids these payments. The luxury and cosmetics financial factbook 2016

Luxury and Cosmetic Financial Factbook Page 58 Page 60

Luxury and Cosmetic Financial Factbook Page 58 Page 60