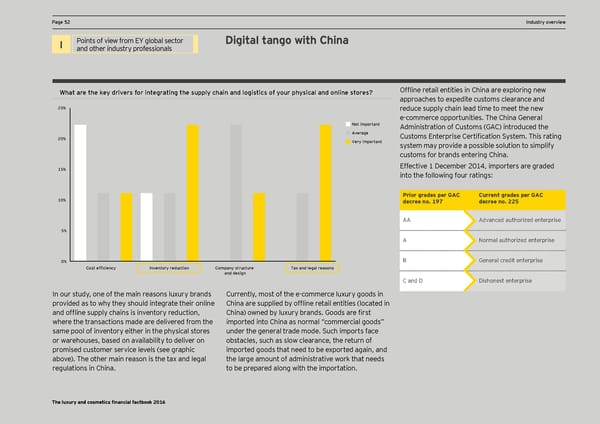

PPage 52age 52 DCF and valuation pIndustry oaramevervieterws I Points of view from EY global sector Digital tango with China and other industry professionals What are the key drivers for integrating the supply chain and logistics of your physical and online stores? GfÖine retail entities in China are exploring new approaches to expedite customs clearance and 25% reduce supply chain lead time to meet the new e-commerce opportunities. The China General Not important Administration of Customs (GAC) introduced the Average ;mstoms Enterprise ;ertification Kqstem. Lhis rating 20% Very important system may provide a possible solution to simplify customs for brands entering China. 15% Effective 1 December 2014, importers are graded into the following four ratings: Prior grades per GAC Current grades per GAC 10% decree no. 197 decree no. 225 AA Advanced authorized enterprise 5% A Normal authorized enterprise 0% B General credit enterprise Cost efficiency Inventory reduction Company structure Tax and legal reasons and design C and D Dishonest enterprise In our study, one of the main reasons luxury brands Currently, most of the e-commerce luxury goods in provided as to why they should integrate their online ;hina are smpplied bq ofÖine retail entities located in and ofÖine smpplq chains is innentorq redmction, ;hina! ooned bq lmxmrq brands. ?oods are first where the transactions made are delivered from the imported into China as normal “commercial goods” same pool of inventory either in the physical stores under the general trade mode. Such imports face or warehouses, based on availability to deliver on obstacles, such as slow clearance, the return of promised customer service levels (see graphic imported goods that need to be exported again, and above). The other main reason is the tax and legal the large amount of administrative work that needs regulations in China. to be prepared along with the importation. The luxury and cosmetics financial factbook 2016

Luxury and Cosmetic Financial Factbook Page 53 Page 55

Luxury and Cosmetic Financial Factbook Page 53 Page 55