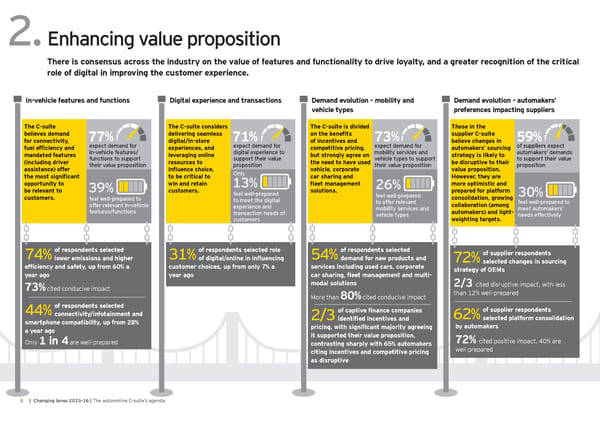

2.Enhancing value proposition There is consensus across the industry on the value of features and functionality to drive loyalty, and a greater recognition of the critical role of digital in improving the customer experience. In-vehicle features and functions Digital experience and transactions Demand evolution - mobility and Demand evolution - automakers’ vehicle types preferences impacting suppliers The C-suite The C-suite considers The C-suite is divided Those in the believes demand 77% delivering seamless 71% on the benefi ts 73% supplier C-suite 59% for connectivity, expect demand for digital/in-store expect demand for of incentives and expect demand for believe changes in of suppliers expect fuel effi ciency and in-vehicle features/ experiences, and digital experience to competitive pricing, mobility services and automakers’ sourcing automakers’ demands mandated features functions to support leveraging online support their value but strongly agree on vehicle types to support strategy is likely to to support their value (including driver their value proposition resources to proposition the need to have used their value proposition be disruptive to their proposition assistance) offer infl uence choice, Only vehicle, corporate value proposition. the most signifi cant to be critical to car sharing and However, they are opportunity to 39% win and retain 13% fl eet management 26% more optimistic and be relevant to customers. feel well-prepared solutions. feel well-prepared prepared for platform 30% customers. feel well-prepared to to meet the digital to offer relevant consolidation, growing feel well-prepared to offer relevant in-vehicle experience and mobility services and collaboration (among meet automakers’ features/functions transaction needs of vehicle types automakers) and light- needs effectively customers weighting targets. 74%of respondents selected 31%of respondents selected role 54%of respondents selected of supplier respondents lower emissions and higher of digital/online in infl uencing demand for new products and 72%selected changes in sourcing effi ciency and safety, up from 60% a customer choices, up from only 7% a services including used cars, corporate strategy of OEMs year ago year ago car sharing, fl eet management and multi- 73% cited conducive impact modal solutions 2/3 cited disruptive impact, with less More than 80% cited conducive impact than 12% well-prepared 44%of respondents selected of captive fi nance companies of supplier respondents connectivity/infotainment and 2/3identifi ed incentives and 62%selected platform consolidation smartphone compatibility, up from 28% pricing, with signifi cant majority agreeing by automakers a year ago it supported their value proposition, 72% cited positive impact, 40% are Only 1 in 4 are well-prepared contrasting sharply with 65% automakers citing incentives and competitive pricing well-prepared as disruptive 6 | Changing lanes 2015-16 | The automotive C-suite’s agenda

Changing Lanes Page 5 Page 7

Changing Lanes Page 5 Page 7