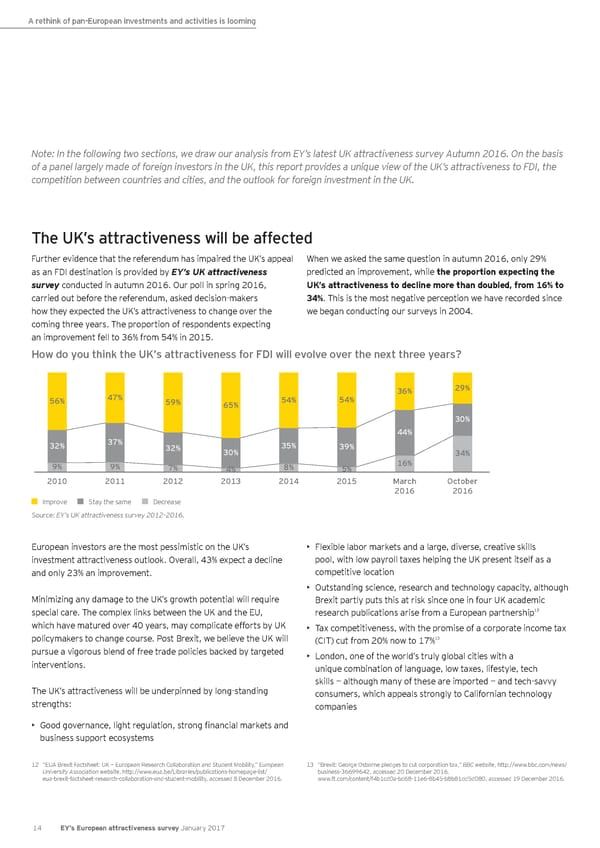

A rethink of pan-European investments and activities is looming Note: In the following two sections, we draw our analysis from EY’s latest UK attractiveness survey Autumn 2016. On the basis of a panel largely made of foreign investors in the UK, this report provides a unique view of the UK’s attractiveness to FDI, the competition between countries and cities, and the outlook for foreign investment in the UK. The UK’s attractiveness will be affected Further evidence that the referendum has impaired the UK’s appeal When we asked the same question in autumn 2016, only 29% as an FDI destination is provided by EY’s UK attractiveness predicted an improvement, while the proportion expecting the survey conducted in autumn 2016. Our poll in spring 2016, UK’s attractiveness to decline more than doubled, from 16% to carried out before the referendum, asked decision-makers 34%. This is the most negative perception we have recorded since how they expected the UK’s attractiveness to change over the we began conducting our surveys in 2004. coming three years. The proportion of respondents expecting an improvement fell to 36% from 54% in 2015. How do you think the UK’s attractiveness for FDI will evolve over the next three years? 36% 29% 56% 47% 59% 65% 54% 54% 30% 44% 32% 37% 32% 35% 39% 30% 34% 9% 9% 7% 4% 8% 5% 16% 2010 2011 2012 2013 2014 2015 March October 2016 2016 Improve Stay the same Decrease Source: EY’s UK attractiveness survey 2012–2016. European investors are the most pessimistic on the UK’s • Flexible labor markets and a large, diverse, creative skills investment attractiveness outlook. Overall, 43% expect a decline pool, with low payroll taxes helping the UK present itself as a and only 23% an improvement. competitive location • Outstanding science, research and technology capacity, although Minimizing any damage to the UK’s growth potential will require Brexit partly puts this at risk since one in four UK academic special care. The complex links between the UK and the EU, 12 research publications arise from a European partnership which have matured over 40 years, may complicate efforts by UK • Tax competitiveness, with the promise of a corporate income tax policymakers to change course. Post Brexit, we believe the UK will 13 (CIT) cut from 20% now to 17% pursue a vigorous blend of free trade policies backed by targeted • London, one of the world’s truly global cities with a interventions. unique combination of language, low taxes, lifestyle, tech skills — although many of these are imported — and tech-savvy The UK’s attractiveness will be underpinned by long-standing consumers, which appeals strongly to Californian technology strengths: companies • Good governance, light regulation, strong financial markets and business support ecosystems 12 “EUA Brexit Factsheet: UK — European Research Collaboration and Student Mobility,” European 13 “Brexit: George Osborne pledges to cut corporation tax,” BBC website, http://www.bbc.com/news/ University Association website, http://www.eua.be/Libraries/publications-homepage-list/ business-36699642, accessed 20 December 2016. eua-brexit-factsheet-research-collaboration-and-student-mobility, accessed 8 December 2016. www.ft.com/content/f4b1cd0a-bd68-11e6-8b45-b8b81dd5d080, accessed 19 December 2016. 14 EY’s European attractiveness survey January 2017

European attractiveness survey January 2017 Page 18 Page 20

European attractiveness survey January 2017 Page 18 Page 20