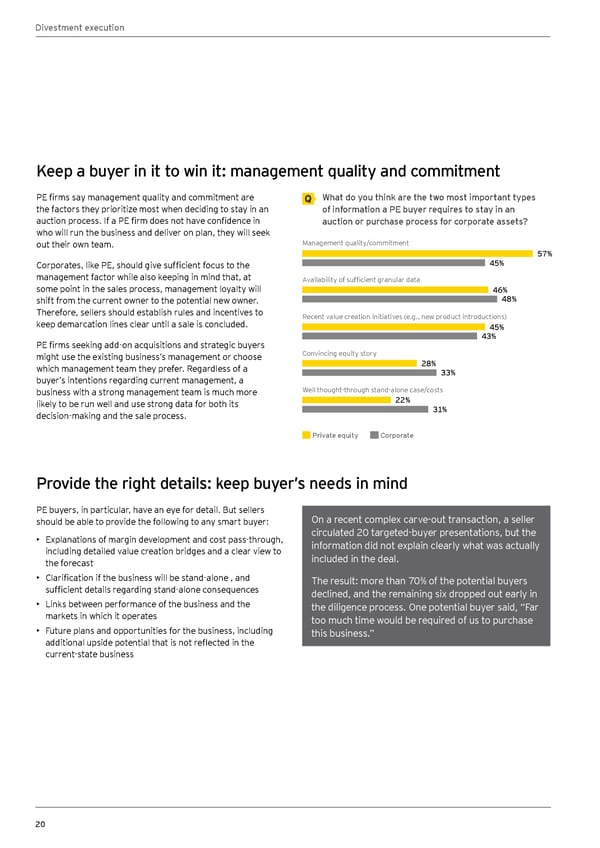

Divestment execution Keep a buyer in it to win it: management quality and commitment PE firms say management quality and commitment are What do you think are the two most important types the factors they prioritize most when deciding to stay in an of information a PE buyer requires to stay in an auction process. If a PE firm does not have confidence in auction or purchase process for corporate assets? who will run the business and deliver on plan, they will seek out their own team. Management quality/commitment 57% Corporates, like PE, should give sufficient focus to the 45% management factor while also keeping in mind that, at Availability of sufficient granular data some point in the sales process, management loyalty will 46% shift from the current owner to the potential new owner. 48% Therefore, sellers should establish rules and incentives to Recent value creation initiatives (e.g., new product introductions) keep demarcation lines clear until a sale is concluded. 45% 43% PE firms seeking add-on acquisitions and strategic buyers might use the existing business’s management or choose Convincing equity story which management team they prefer. Regardless of a 28% buyer’s intentions regarding current management, a 33% business with a strong management team is much more Well thought-through stand-alone case/costs likely to be run well and use strong data for both its 22% decision-making and the sale process. 31% Private equity Corporate Provide the right details: keep buyer’s needs in mind PE buyers, in particular, have an eye for detail. But sellers On a recent complex carve-out transaction, a seller should be able to provide the following to any smart buyer: • Explanations of margin development and cost pass-through, circulated 20 targeted-buyer presentations, but the including detailed value creation bridges and a clear view to information did not explain clearly what was actually the forecast included in the deal. • Clarification if the business will be stand-alone , and The result: more than 70% of the potential buyers sufficient details regarding stand-alone consequences declined, and the remaining six dropped out early in • Links between performance of the business and the the diligence process. One potential buyer said, “Far markets in which it operates too much time would be required of us to purchase • Future plans and opportunities for the business, including this business.” additional upside potential that is not reflected in the current-state business 20

Global Corporate Divestment Study Page 19 Page 21

Global Corporate Divestment Study Page 19 Page 21