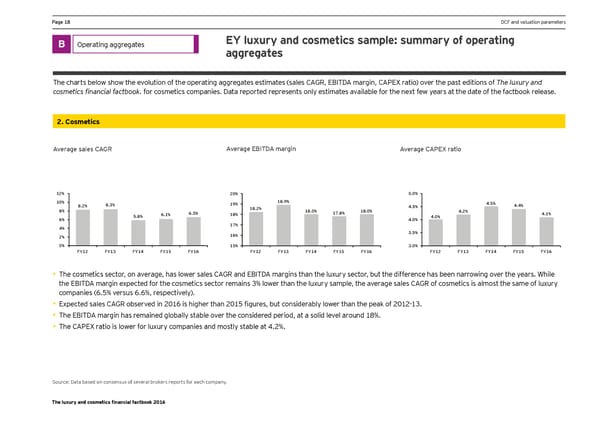

Ha_e )0 DCF and valuation parameters B Operating aggregates EY luxury and cosmetics sample: summary of operating aggregates The charts below show the evolution of the operating aggregates estimates (sales CAGR, EBITDA margin, CAPEX ratio) over the past editions of The luxury and cosmetics financial factbook. for cosmetics companies. Data reported represents only estimates available for the next few years at the date of the factbook release. 2. Cosmetics Average sales CAGR Average EBITDA margin Average CAPEX ratio 12% 20% 5.0% 10% 8.3% 19% 18.9% 4.5% 4.4% 8.2% 18.2% 4.5% 8% 6.1% 6.5% 18% 18.0% 17.8% 18.0% 4.2% 4.1% 6% 5.8% 4.0% 4.0% 4% 17% 16% 3.5% 2% 0% 15% 3.0% FY12 FY13 FY14 FY15 FY16 FY12 FY13 FY14 FY15 FY16 FY12 FY13 FY14 FY15 FY16 • The cosmetics sector, on average, has lower sales CAGR and EBITDA margins than the luxury sector, but the difference has been narrowing over the years. While the EBITDA margin expected for the cosmetics sector remains 3% lower than the luxury sample, the average sales CAGR of cosmetics is almost the same of luxury companies (6.5% versus 6.6%, respectively). • Expected sales ;9?J obserned in *(). is higher than *()- figmres, bmt considerablq looer than the peac of *()*%)+. • The EBITDA margin has remained globally stable over the considered period, at a solid level around 18%. • The CAPEX ratio is lower for luxury companies and mostly stable at 4.2%. Source: Data based on consensus of several brokers reports for each company. The luxury and cosmetics financial factbook 2016

Luxury and Cosmetic Financial Factbook Page 19 Page 21

Luxury and Cosmetic Financial Factbook Page 19 Page 21