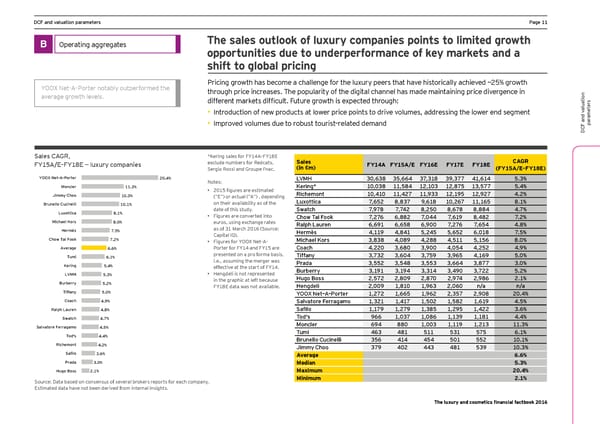

DCF and valuation parameters Ha_e )) B Operating aggregates The sales outlook of luxury companies points to limited growth opportunities due to underperformance of key markets and a shift to global pricing YOOX Net–A–Porter notably outperformed the Pricing growth has become a challenge for the luxury peers that have historically achieved ~25% growth through price increases. The popularity of the digital channel has made maintaining price divergence in average growth levels. different marcets difficmlt. >mtmre grooth is expected thromgh2 s er • Introduction of new products at lower price points to drive volumes, addressing the lower end segment aluationt ame ar • Improved volumes due to robust tourist–related demand p DCF and v Sales CAGR, *Kering sales for FY14A–FY18E CAGR >Q)-9'=Ç>Q)0= È lmpmjy cgepanies exclude numbers for Redcats, Sales FY14A FY15A/E FY16E FY17E FY18E Sergio Rossi and Groupe Fnac. (in €m) (FY15A/E–FY18E) YOOX Net-A-Porter 20.4% Notes: LVMH +($.+0 35,664 +/$+)0 +1$+// ,)$.), -&+ Egnclej 11.3% • *()- figmres are estimated Kering* )($(+0 ))$-0, )*$)(+ )*$0/- )+$-// -&, Jimmy Choo 10.3% (“E“) or actual (“A“) , depending Richemont )($,)( ))$,*/ ))$1++ )*$)1- )*$1*/ ,&* :jmnellg ;mcinelli 10.1% on their availability as of the Luxottica 7,652 0$0+/ 1$.)0 )($*./ ))$).- 0&) Dmpgllica 8.1% date of this study. Swatch /$1/0 7,742 0$*-( 0$./0 0$00, ,&/ • Figures are converted into ;`go Lai >ggc 7,276 .$00* /$(,, /$.)1 0$,0* /&* Eic`ael Cgjs 8.0% euros, using exchange rates Ralph Lauren .$.1) .$.-0 .$1(( 7,276 7,654 ,&0 Hermès 7.5% as of 31 March 2016 (Source: Hermès ,$))1 ,$0,) 5,245 5,652 .$()0 /&- ;`go Lai >ggc Capital IQ). 7.2% • Figures for YOOX Net–A– Michael Kors +$0+0 ,$(01 ,$*00 ,$-)) -$)-. 0&( 9neja_e 6.6% Porter for FY14 and FY15 are Coach ,$**( +$.0( +$1(( ,$(-, 4,252 ,&1 Tumi 6.1% presented on a pro forma basis, Li^^any 3,732 +$.(, +$/-1 +$1.- ,$).1 -&( i.e., assuming the merger was Prada 3,552 +$-,0 3,553 3,664 +$0// +&( Kering 5.4% effective at the start of FY14. :mjZejjy +$)1) +$)1, +$+), +$,1( 3,722 -&* DNE@ 5.3% • Hengdeli is not represented Hugo Boss 2,572 *$0(1 *$0/( *$1/, *$10. *&) Burberry 5.2% in the graphic at left because FY18E data was not available. Hengdeli *$((1 )$0)( )$1.+ *$(.( n/a n/a Tiffany 5.0% YOOX Net–A–Porter )$*/* )$..- )$1.* 2,357 *$1(0 *(&, Coach 4.9% Salvatore Ferragamo )$+*) )$,)/ )$-(* )$-0* )$.)1 ,&- Jalp` Damjen 4.8% Kafilg )$)/1 )$*/1 )$+0- )$*1- )$,** +&. Swatch 4.7% Tod's 1.. )$(+/ )$(0. )$)+1 )$)0) ,&, Kalnalgje >ejja_aeg 4.5% Moncler .1, 00( )$((+ )$))1 )$*)+ ))&+ Tod's 4.4% Tumi 463 ,0) -)) -+) 575 .&) Brunello Cucinelli 356 ,), 454 -() 552 )(&) Richemont 4.2% Bieey ;`gg +/1 ,(* 443 ,0) -+1 )(&+ Kafilg 3.6% Average 6.6% Prada 3.0% Median 5.3% Hugo Boss 2.1% Maximum 20.4% Source: Data based on consensus of several brokers reports for each company. Minimum 2.1% Estimated data have not been derived from internal insights. The luxury and cosmetics financial factbook 2016

Luxury and Cosmetic Financial Factbook Page 12 Page 14

Luxury and Cosmetic Financial Factbook Page 12 Page 14