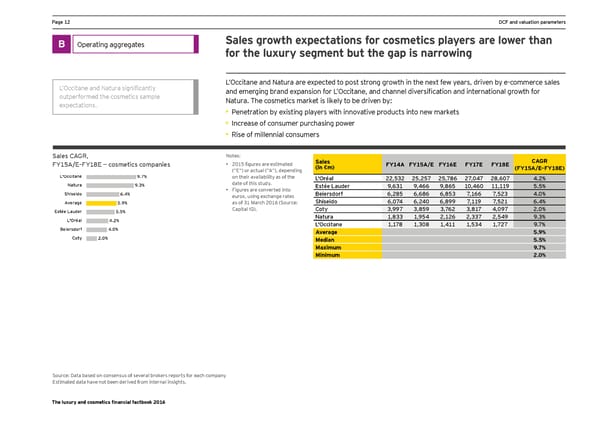

Ha_e )* DCF and valuation parameters Hermès 35.5% B Operating aggregates Sales growth expectations for cosmetics players are lower than Moncler 33.6% for the luxury segment but the gap is narrowing Michael Kors 29.0% Richemont 26.7% Tiffany 25.1% Prada 24.7% D’Gccitane and Fatmra significantlq L’Occitane and Natura are expected to post strong growth in the next few years, driven by e-commerce sales Coach 24.0% outperformed the cosmetics sample and emerging brand expansion for D’Gccitane, and channel dinersification and international grooth for Salvatore Ferragamo 23.5% expectations. Natura. The cosmetics market is likely to be driven by: LVMH 23.2% • Penetration by existing players with innovative products into new markets Swatch 23.1% • Increase of consumer purchasing power Luxottica 22.9% Tod's 21.3% • Rise of millennial consumers Hugo Boss 21.1% Sales CAGR, Notes: Average 21.0% Burberry Sales 20.9% CAGR >Q)-9'=Ç>Q)0= È cgseelics cgepanies • *()- figmres are estimated (in €m) FY14A FY15A/E FY16E FY17E FY18E (FY15A/E–FY18E) Tumi 20.5% (“E“) or actual (“A“), depending L'Occitane 9.7% on their availability as of the Kering L'Oréal 19.1% 22,532 25,257 *-$/0. */$(,/ *0$.(/ ,&* Natura 9.3% date of this study. Estée Lauder 1$.+) 1$,.. 1$0.- )($,.( ))$))1 -&- Brunello Cucinelli 17.3% Shiseido 6.4% • Figures are converted into :eiejsdgj^ .$*0- .$.0. .$0-+ /$).. 7,523 ,&( Ralph Lauren 17.1% euros, using exchange rates Shiseido .$(/, .$*,( .$011 /$))1 /$-*) .&, Average 5.9% as of 31 March 2016 (Source: Jimmy Choo 16.8% Estée Lauder 5.5% Capital IQ). Chow Tai Fook Coty 10.9% +$11/ +$0-1 3,762 +$0)/ ,$(1/ *&( L'Oréal 4.2% Natura )$0++ )$1-, *$)*. 2,337 *$-,1 1&+ Kafilg 9.8% L'Occitane )$)/0 )$+(0 )$,)) )$-+, )$/*/ 1&/ Beiersdorf 4.0% YOOX Net-A-Porter 9.5% Average 5.9% Coty 2.0% Hengdeli 7.5% Median 5.5% Maximum 9.7% Minimum 2.0% Source: Data based on consensus of several brokers reports for each company Estimated data have not been derived from internal insights. The luxury and cosmetics financial factbook 2016

Luxury and Cosmetic Financial Factbook Page 13 Page 15

Luxury and Cosmetic Financial Factbook Page 13 Page 15