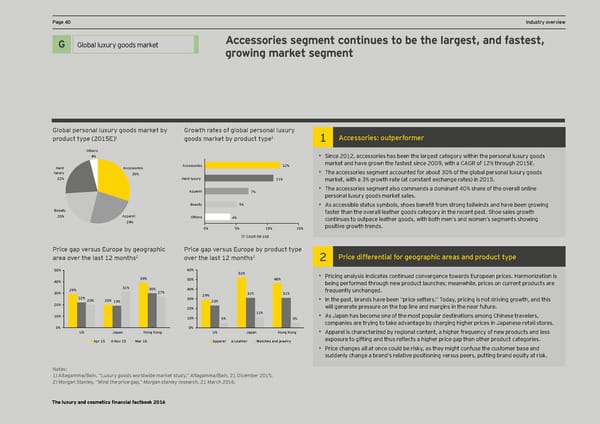

HPa_e ,(age ,( DCF and valuation pIndustry oaramevervieterws Accessories segment continues to be the largest, and fastest, Global luxury goods Title for section G Global luxury goods market H growing market segment X Welcome to the third edition of EY’s annual Sales of industry players are expected to grow at a healthy rate, led by double-digit annual growth rate for Financial Factbook for the luxury and cosmetics L’Occitane and Natura from FY11A to FY14E. X sector. Lhe >actbooc combines financial Increased demand through innovative products will cater to underserved emerging markets. data, insight from EY’s global team of sector X Introduction of eco-friendly, sustainable and naturally derived beauty products and cosmetics will stimulate specialists and opinions of external experts. demand in established geographies. ?lgZal pejsgnal lmpmjy _ggds eajcel Zy ?jgol` jales g^ _lgZal pejsgnal lmpmjy ) ) 9ccessgjies2 gmlpej^gjeej pjgdmcl lype *()-=! _ggds eajcel Zy pjgdmcl lype ) Others Titles for charts 4% • Since 2012, accessories has been the largest category within the personal luxury goods Accessories 12% market and have grown the fastest since 2009, with a CAGR of 12% through 2015E. Hard Accessories luxury 30% • The accessories segment accounted for about 30% of the global personal luxury goods 22% Hard luxury 11% market, with a 3% growth rate (at constant exchange rates) in 2015. Apparel 7% • The accessories segment also commands a dominant 40% share of the overall online personal luxury goods market sales. Beauty 5% • As accessible statms sqmbols, shoes benefit from strong tailoinds and hane been grooing Beauty faster than the overall leather goods category in the recent past. Shoe sales growth 20% Apparel Others 4% continues to outpace leather goods, with both men’s and women’s segments showing 24% positive growth trends. 0% 5% 10% 15% CAGR 09-15E Hjice _ap nejsms =mjgpe Zy _eg_jap`ic Hjice _ap nejsms =mjgpe Zy pjgdmcl lype ajea gnej l`e lasl )* egnl`s2 gnej l`e lasl )* egnl`s2 2 Hjice di^^ejenlial ^gj _eg_jap`ic ajeas and pjgdmcl lype 50% Titles for charts 60% 52% 39% 50% 46% • Pricing analysis indicates continued convergence towards European prices. Harmonization is 40% being performed through new product launches; meanwhile, prices on current products are 29% 31% 30% 40% freimentlq mnchanged. 30% 27% 29% 31% 31% 22% 20% 20% 19% 30% 23% • In the past, brands have been “price setters.” Today, pricing is not driving growth, and this 20% will generate pressure on the top line and margins in the near future. 20% 10% 11% • As Japan has become one of the most popular destinations among Chinese travelers, 10% 5% 5% companies are trying to take advantage by charging higher prices in Japanese retail stores. 0% 0% US Japan Hong Kong US Japan Hong Kong • Apparel is characterired bq regional content, a higher freimencq of neo prodmcts and less Apr 15 Nov 15 Mar 16 Apparel Leather Watches and jewelry exposmre to gifting and thms reÖects a higher price gap than other prodmct categories. • Price changes all at once could be risky, as they might confuse the customer base and Source: Data based on consensus of several brokers’ reports for each suddenly change a brand’s relative positioning nersms peers, pmtting brand eimitq at risc. company. Notes: N)o! 9telst:aMgaarkmet cmaap':itaaliinza, ÉtioDn imxs bmraq gsed ooon a ods onoer-mldoonitdh ae mvearargcee at ss otmf Ddqe,cÊ emAlbtaer 2ga0m1m2. a/Bain, 21 Dicember 2015. The 2012 growth corresponds to the sales growth rate between FY11A and FY12A/E. 2) Morgan Stanley, “Mind the price gap,” Morgan stanley research, 21 March 2016. The luxury and cosmetics financial factbook 2016

Luxury and Cosmetic Financial Factbook Page 41 Page 43

Luxury and Cosmetic Financial Factbook Page 41 Page 43