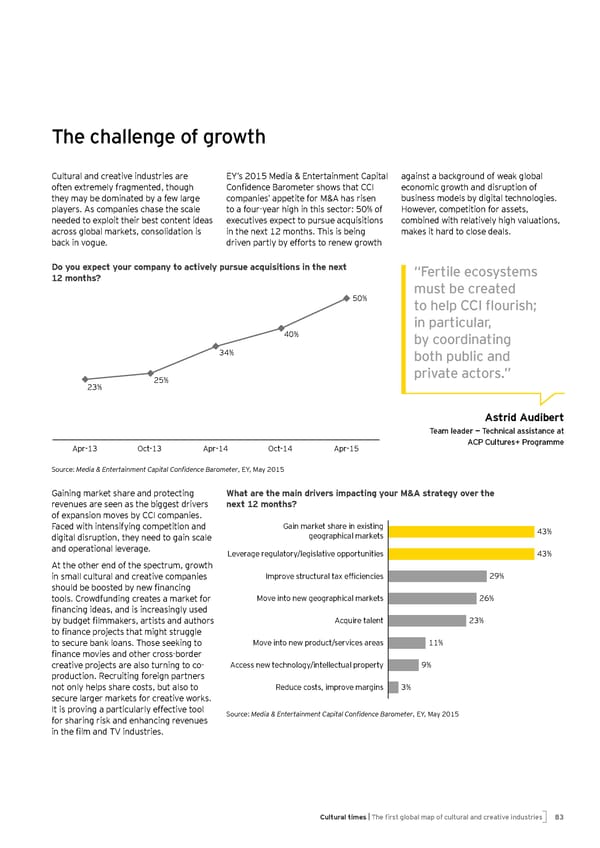

L`e c`adden_e o^ _root` Cu lt u ral and creat ive indu st ries are E Y ’ s 2 0 1 5 M edia & E nt ert ainment Capit al against a b ack grou nd of w eak glob al oft en ex t remely fragment ed, t h ou gh ;onfidence :aroeeter k`ook t`at ;;A economic grow t h and disru pt ion of t h ey may b e dominat ed b y a few large companies’ appet it e for M & A h as risen b u siness models b y digit al t ech nologies. play ers. As companies ch ase t h e scale t o a fou r- y ear h igh in t h is sect or: 5 0 % of H ow ever, compet it ion for asset s, needed t o ex ploit t h eir b est cont ent ideas ex ecu t ives ex pect t o pu rsu e acq u isit ions comb ined w it h relat ively h igh valu at ions, across glob al mark et s, consolidat ion is in t h e nex t 1 2 mont h s. T h is is b eing mak es it h ard t o close deals. b ack in vogu e. driven part ly b y effort s t o renew grow t h Do you ex p ect your comp any to actively p ursue acq uisitions in the nex t É>ertide ecosqstees 1 2 months? eust be create\ 5 0 % to `edh ;;A flouris`3 in harticudar$ 4 0 % bq coor\inatin_ 3 4 % bot` hubdic an\ 2 5 % hrinate actors&Ê 2 3 % A strid A udibert Team leader — Technical assistance at Apr- 1 3 O ct - 1 3 Apr- 1 4 O ct - 1 4 Apr- 1 5 ACP Cultures+ Programme S ou rce: Media & Entertainment Capital Confidence Barometer, E Y , M ay 2 0 1 5 G aining mark et sh are and prot ect ing W hat are the main drivers imp acting your M & A strategy over the revenu es are seen as t h e b iggest drivers nex t 1 2 months? of ex pansion moves b y CCI companies. F aced w it h int ensify ing compet it ion and G ain mark et sh are in ex ist ing 4 3 % digit al disru pt ion, t h ey need t o gain scale geograph ical mark et s and operat ional leverage. Leverage regu lat ory / legislat ive opport u nit ies 4 3 % At t h e ot h er end of t h e spect ru m, grow t h in small cu lt u ral and creat ive companies Aehrove ktrmctmral tap efficienciek 2 9 % k`omld Ze Zookted Zy neo financin_ t ools. Crow dfu nding creat es a mark et for M ove int o new geograph ical mark et s 2 6 % financin_ ideak$ and ik increakin_ly mked Zy Zmd_et fileeacerk$ artiktk and amt`ork Acq u ire t alent 2 3 % to finance hrobectk t`at ei_`t ktrm__le t o secu re b ank loans. T h ose seek ing t o M ove int o new produ ct / services areas 1 1 % finance eoviek and ot`er crokk%Zorder creat ive proj ect s are also t u rning t o co- Access new t ech nology / int ellect u al propert y 9 % produ ct ion. R ecru it ing foreign part ners not only h elps sh are cost s, b u t also t o R edu ce cost s, improve margins 3 % secu re larger mark et s for creat ive w ork s. It is proving a part icu larly effect ive t ool S ou rce: Media & Entertainment Capital Confidence Barometer, E Y , M ay 2 0 1 5 for sh aring risk and enh ancing revenu es in t`e file and LN indmktriek& | Cultural times L`e Õrst _dobad eah o^ cudturad an\ creatine in\ustries 8 3

Cultural Times Page 91 Page 93

Cultural Times Page 91 Page 93