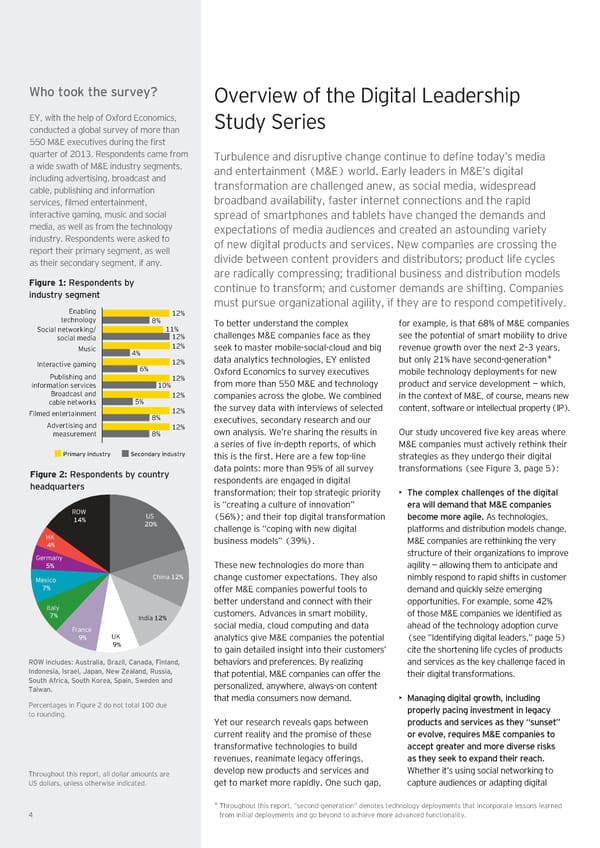

„ho too‚ the surey… ƒvervie‚ o the ¦igital Leadership EY€ ‚ith the help o ƒord Economics€ tudy eries conducted a global survey o more than „„… M&E eecutives during the first uarter o ‡…ˆ‰Š ‹espondents came rom Turbulence and disruptive change continue to define today’s media a ‚ide s‚ath o M&E industry segments€ and entertainment ˜M&Eš ‚orldŠ Early leaders in M&E’s digital including advertising€ broadcast and transormation are challenged ane‚€ as social media€ ‚idespread cable€ publishing and inormation services€ filmed entertainment€ broadband availability€ aster internet connections and the rapid interactive gaming€ music and social spread o smartphones and tablets have changed the demands and media€ as ‚ell as rom the technology epectations o media audiences and created an astounding variety industryŠ ‹espondents ‚ere asŒed to o ne‚ digital products and servicesŠ e‚ companies are crossing the report their primary segment€ as ‚ell divide bet‚een content providers and distributors• product lie cycles as their secondary segment€ i anyŠ are radically compressing• traditional business and distribution models Figure 1: Žespondents by continue to transorm• and customer demands are shitingŠ Companies industry segment must pursue organiœational agility€ i they are to respond competitivelyŠ Enabling 12% technology 8% To better understand the comple or eample€ is that ™ž” o M&E companies Social networking/ 11% challenges M&E companies ace as they see the potential o smart mobility to drive social media 12% Music 12% seeŒ to master mobilesocialcloud and big revenue gro‚th over the net ‡–‰ years€ 4% data analytics technologies€ EY enlisted but only ‡ˆ” have secondgeneration Interactive gaming 12% ¡ 6% ƒord Economics to survey eecutives mobile technology deployments or ne‚ Publishing and 12% rom more than „„… M&E and technology product and service development — ‚hich€ information services 10% Broadcast and 12% companies across the globeŠ Že combined in the contet o M&E€ o course€ means ne‚ cable networks 5% the survey data ‚ith intervie‚s o selected content€ sot‚are or intellectual property ˜I£šŠ Filmed entertainment 12% 8% eecutives€ secondary research and our Advertising and 12% o‚n analysisŠ Že’re sharing the results in ƒur study uncovered five Œey areas ‚here measurement 8% a series o five indepth reports€ o ‚hich M&E companies must actively rethinŒ their Primary industry Secondary industry this is the firstŠ ‘ere are a e‚ topline strategies as they undergo their digital Figure 2: Žespondents by country data points’ more than “„” o all survey transormations ˜see Figure ‰€ page „š’ headŒuarters respondents are engaged in digital transormation• their top strategic priority • The comple‡ challenges of the digital is “creating a culture o innovation” era ill demand that M&E companies ROW US ˜„™”š• and their top digital transormation become more agileˆ As technologies€ 14% 20% challenge is “coping ‚ith ne‚ digital platorms and distribution models change€ HK business models” ˜‰“”šŠ M&E companies are rethinŒing the very 4% Germany structure o their organiœations to improve 5% These ne‚ technologies do more than agility — allo‚ing them to anticipate and Mexico China 12% change customer epectationsŠ They also nimbly respond to rapid shits in customer 7% oer M&E companies po‚erul tools to demand and uicŒly seiœe emerging Italy better understand and connect ‚ith their opportunitiesŠ For eample€ some ¥‡” 7% India 12% customersŠ Advances in smart mobility€ o those M&E companies ‚e identified as France social media€ cloud computing and data ahead o the technology adoption curve 9% UK analytics give M&E companies the potential ˜see “Identiying digital leaders€” page „š 9% to gain detailed insight into their customers’ cite the shortening lie cycles o products Ž„ includes€ ƒustralia‰ ‘rail‰ Canada‰ ’inland‰ behaviors and preerencesŠ ›y realiœing and services as the Œey challenge aced in “ndonesia‰ “srael‰ ”apan‰ •e –ealand‰ Žussia‰ that potential€ M&E companies can oer the their digital transormationsŠ South ƒfrica‰ South —orea‰ Spain‰ Seden and personaliœed€ any‚here€ al‚ayson content Taianˆ that media consumers no‚ demandŠ • Managing digital groth‰ including £ercentages in Figure ‡ do not total ˆ…… due properly pacing inestment in legacy to roundingŠ Yet our research reveals gaps bet‚een products and serices as they “sunset” current reality and the promise o these or eole‰ reŒuires M&E companies to transormative technologies to build accept greater and more dierse ris‚s revenues€ reanimate legacy oerings€ as they see‚ to e‡pand their reachˆ Throughout this report€ all dollar amounts are develop ne‚ products and services and Žhether it’s using social net‚orŒing to § dollars€ unless other‚ise indicatedŠ get to marŒet more rapidlyŠ ƒne such gap€ capture audiences or adapting digital Throughout this report€ “secondgeneration” denotes technology deployments that incorporate lessons learned ¡ † rom initial deployments and go beyond to achieve more advanced unctionalityŠ

Digital Agility Now Page 3 Page 5

Digital Agility Now Page 3 Page 5