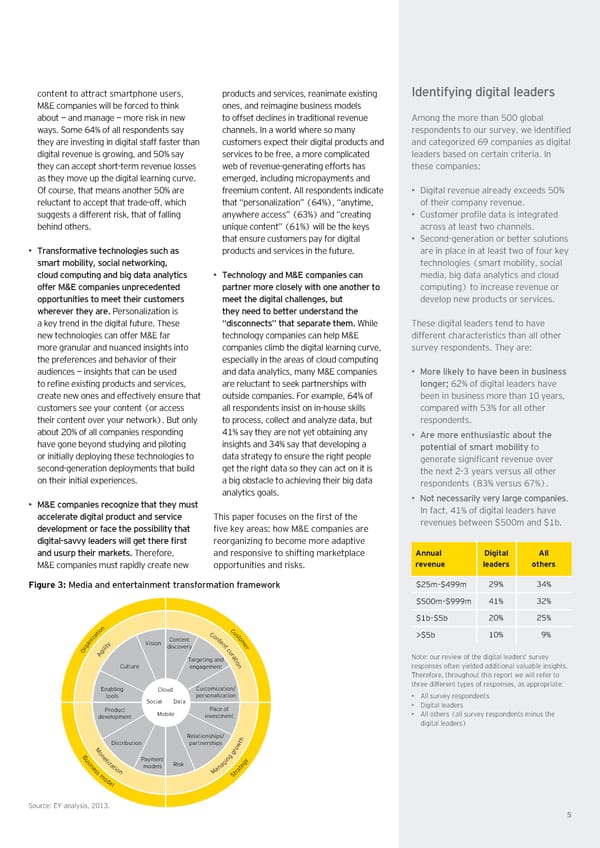

content to attract smartphone users€ products and services€ reanimate eisting “dentifying digital leaders M&E companies ‚ill be orced to thinŒ ones€ and reimagine business models about — and manage — more risŒ in ne‚ to oset declines in traditional revenue Among the more than „…… global ‚aysŠ ome ™¥” o all respondents say channelsŠ In a ‚orld ‚here so many respondents to our survey€ ‚e identified they are investing in digital sta aster than customers epect their digital products and and categoriœed ™“ companies as digital digital revenue is gro‚ing€ and „…” say services to be ree€ a more complicated leaders based on certain criteriaŠ In they can accept shortterm revenue losses ‚eb o revenuegenerating eorts has these companies’ as they move up the digital learning curveŠ emerged€ including micropayments and ƒ course€ that means another „…” are reemium contentŠ All respondents indicate • ¦igital revenue already eceeds „…” reluctant to accept that tradeo€ ‚hich that “personaliœation” ˜™¥”š€ “anytime€ o their company revenueŠ suggests a dierent risŒ€ that o alling any‚here access” ˜™‰”š and “creating • Customer profile data is integrated behind othersŠ uniue content” ˜™ˆ”š ‚ill be the Œeys across at least t‚o channelsŠ that ensure customers pay or digital • econdgeneration or better solutions • Transformatie technologies such as products and services in the utureŠ are in place in at least t‚o o our Œey smart mobility‰ social netor‚ing‰ technologies ˜smart mobility€ social cloud computing and big data analytics • Technology and M&E companies can media€ big data analytics and cloud offer M&E companies unprecedented partner more closely ith one another to computingš to increase revenue or opportunities to meet their customers meet the digital challenges‰ but develop ne‚ products or servicesŠ hereer they areˆ £ersonaliœation is they need to better understand the a Œey trend in the digital utureŠ These “disconnects” that separate themˆ Žhile These digital leaders tend to have ne‚ technologies can oer M&E ar technology companies can help M&E dierent characteristics than all other more granular and nuanced insights into companies climb the digital learning curve€ survey respondentsŠ They are’ the preerences and behavior o their especially in the areas o cloud computing audiences — insights that can be used and data analytics€ many M&E companies • More li‚ely to hae been in business to refine eisting products and services€ are reluctant to seeŒ partnerships ‚ith longer™ ™‡” o digital leaders have create ne‚ ones and eectively ensure that outside companiesŠ For eample€ ™¥” o been in business more than ˆ… years€ customers see your content ˜or access all respondents insist on inhouse sŒills compared ‚ith „‰” or all other their content over your net‚orŒšŠ ›ut only to process€ collect and analyœe data€ but respondentsŠ about ‡…” o all companies responding ¥ˆ” say they are not yet obtaining any • ƒre more enthusiastic about the have gone beyond studying and piloting insights and ‰¥” say that developing a potential of smart mobility to or initially deploying these technologies to data strategy to ensure the right people generate significant revenue over secondgeneration deployments that build get the right data so they can act on it is the net ‡‰ years versus all other on their initial eperiencesŠ a big obstacle to achieving their big data respondents ˜ž‰” versus ™¨”šŠ analytics goalsŠ • •ot necessarily ery large companiesŠ • M&E companies recognie that they must In act€ ¥ˆ” o digital leaders have accelerate digital product and serice This paper ocuses on the first o the revenues bet‚een ©„……m and ©ˆbŠ deelopment or face the possibility that five Œey areas’ ho‚ M&E companies are digitalsay leaders ill get there first reorganiœing to become more adaptive and usurp their mar‚etsˆ Thereore€ and responsive to shiting marŒetplace nnua igita M&E companies must rapidly create ne‚ opportunities and risŒsŠ reenue eader other Figure 3: Media and entertainment transformation frameor‚ ©‡„m–©¥““m ‡“” ‰¥” ©„……m–©“““m ¥ˆ” ‰‡” ©ˆb–©„b ‡…” ‡„” n C o u i t C s ˆ…” “” a o t ª©„b z n o i Content t m n Vision e a y n e g t discovery t r r i l c i u O g r A a t ote’ our revie‚ o the digital leaders’ survey Targeting and i o n Culture engagement responses oten yielded additional valuable insightsŠ Thereore€ throughout this report ‚e ‚ill reer to Enabling Customization/ three dierent types o responses€ as appropriate’ tools Cloud personalization • All survey respondents Social Data • ¦igital leaders Product Mobile Pace of • All others ˜all survey respondents minus the development investment digital leadersš Relationships/ th M Distribution partnerships ow r B one g g usin tiza Payment Risk agin egy es tio models an at s m n M Str ode l ource’ EY analysis€ ‡…ˆ‰Š š

Digital Agility Now Page 4 Page 6

Digital Agility Now Page 4 Page 6