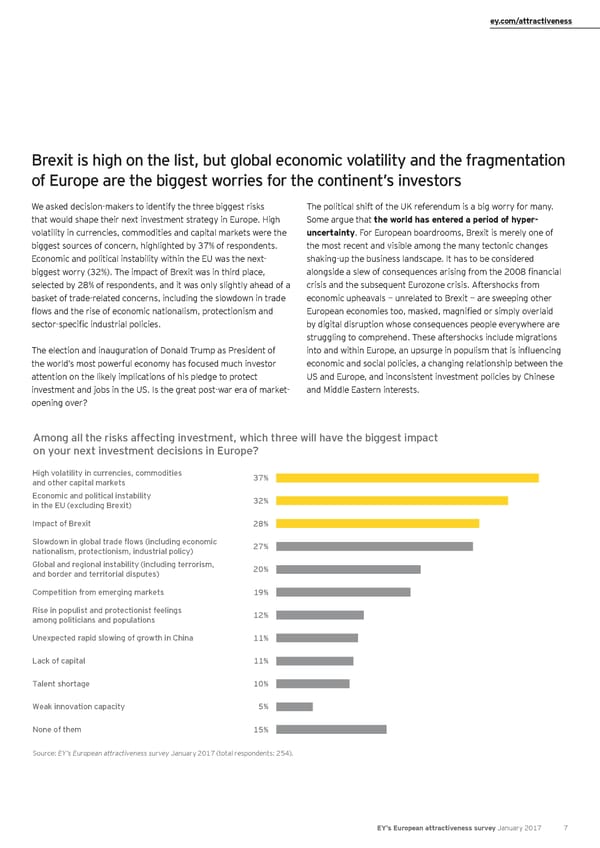

ey.com/attractiveness Brexit is high on the list, but global economic volatility and the fragmentation of Europe are the biggest worries for the continent’s investors We asked decision-makers to identify the three biggest risks The political shift of the UK referendum is a big worry for many. that would shape their next investment strategy in Europe. High Some argue that the world has entered a period of hyper- volatility in currencies, commodities and capital markets were the uncertainty. For European boardrooms, Brexit is merely one of biggest sources of concern, highlighted by 37% of respondents. the most recent and visible among the many tectonic changes Economic and political instability within the EU was the next- shaking-up the business landscape. It has to be considered biggest worry (32%). The impact of Brexit was in third place, alongside a slew of consequences arising from the 2008 financial selected by 28% of respondents, and it was only slightly ahead of a crisis and the subsequent Eurozone crisis. Aftershocks from basket of trade-related concerns, including the slowdown in trade economic upheavals — unrelated to Brexit — are sweeping other flows and the rise of economic nationalism, protectionism and European economies too, masked, magnified or simply overlaid sector-specific industrial policies. by digital disruption whose consequences people everywhere are struggling to comprehend. These aftershocks include migrations The election and inauguration of Donald Trump as President of into and within Europe, an upsurge in populism that is influencing the world’s most powerful economy has focused much investor economic and social policies, a changing relationship between the attention on the likely implications of his pledge to protect US and Europe, and inconsistent investment policies by Chinese investment and jobs in the US. Is the great post-war era of market- and Middle Eastern interests. opening over? Among all the risks affecting investment, which three will have the biggest impact on your next investment decisions in Europe? High volatility in currencies, commodities 37% and other capital markets Economic and political instability 32% in the EU (excluding Brexit) Impact of Brexit 28% Slowdown in global trade flows (including economic 27% nationalism, protectionism, industrial policy) Global and regional instability (including terrorism, 20% and border and territorial disputes) Competition from emerging markets 19% Rise in populist and protectionist feelings 12% among politicians and populations Unexpected rapid slowing of growth in China 11% Lack of capital 11% Talent shortage 10% Weak innovation capacity 5% None of them 15% Source: EY’s European attractiveness survey January 2017 (total respondents: 254). EY’s European attractiveness survey January 2017 7

European attractiveness survey January 2017 Page 10 Page 12

European attractiveness survey January 2017 Page 10 Page 12