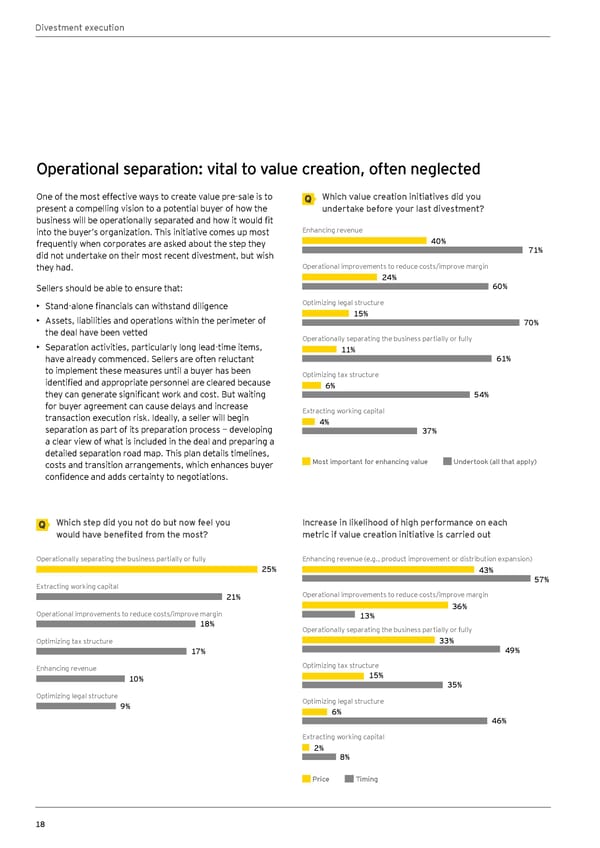

Divestment execution Operational separation: vital to value creation, often neglected One of the most effective ways to create value pre-sale is to Which value creation initiatives did you present a compelling vision to a potential buyer of how the undertake before your last divestment? business will be operationally separated and how it would fit into the buyer’s organization. This initiative comes up most Enhancing revenue frequently when corporates are asked about the step they 40% did not undertake on their most recent divestment, but wish 71% they had. Operational improvements to reduce costs/improve margin 24% Sellers should be able to ensure that: 60% • Stand-alone financials can withstand diligence Optimizing legal structure • Assets, liabilities and operations within the perimeter of 15% 70% the deal have been vetted Operationally separating the business partially or fully • Separation activities, particularly long lead-time items, 11% have already commenced. Sellers are often reluctant 61% to implement these measures until a buyer has been Optimizing tax structure identified and appropriate personnel are cleared because 6% they can generate significant work and cost. But waiting 54% for buyer agreement can cause delays and increase Extracting working capital transaction execution risk. Ideally, a seller will begin 4% separation as part of its preparation process — developing 37% a clear view of what is included in the deal and preparing a detailed separation road map. This plan details timelines, costs and transition arrangements, which enhances buyer Most important for enhancing value Undertook (all that apply) confidence and adds certainty to negotiations. Which step did you not do but now feel you Increase in likelihood of high performance on each would have benefited from the most? metric if value creation initiative is carried out Operationally separating the business partially or fully Enhancing revenue (e.g., product improvement or distribution expansion) 25% 43% Extracting working capital 57% 21% Operational improvements to reduce costs/improve margin 36% Operational improvements to reduce costs/improve margin 13% 18% Operationally separating the business partially or fully Optimizing tax structure 33% 17% 49% Enhancing revenue Optimizing tax structure 10% 15% 35% Optimizing legal structure Optimizing legal structure 9% 6% 46% Extracting working capital 2% 8% Price Timing 18

Global Corporate Divestment Study Page 17 Page 19

Global Corporate Divestment Study Page 17 Page 19