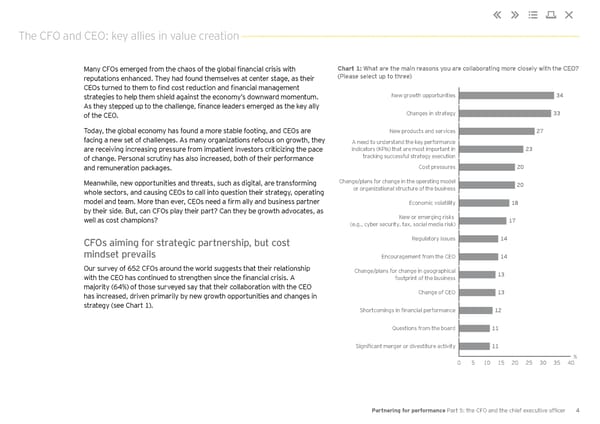

The CFO and CEO: key allies in value creation Many CFOs emerged from the chaos of the global financial crisis with Chart 1: What are the main reasons you are collaborating more closely with the CEO? reputations enhanced. They had found themselves at center stage, as their (Please select up to three) CEOs turned to them to find cost reduction and financial management strategies to help them shield against the economy’s downward momentum. New growth opportunities 34 As they stepped up to the challenge, finance leaders emerged as the key ally of the CEO. Changes in strategy 33 Today, the global economy has found a more stable footing, and CEOs are New products and services 27 facing a new set of challenges. As many organizations refocus on growth, they A need to understand the key performance are receiving increasing pressure from impatient investors criticizing the pace indicators (KPIs) that are most important in 23 of change. Personal scrutiny has also increased, both of their performance tracking successful strategy execution and remuneration packages. Cost pressures 20 Meanwhile, new opportunities and threats, such as digital, are transforming Change/plans for change in the operating model 20 siness whole sectors, and causing CEOs to call into question their strategy, operating or organizational structure of the bu model and team. More than ever, CEOs need a firm ally and business partner Economic volatility 18 by their side. But, can CFOs play their part? Can they be growth advocates, as well as cost champions? New or emerging risks 17 (e.g., cyber security, tax, social media risk) CFOs aiming for strategic partnership, but cost Regulatory issues 14 mindset prevails Encouragement from the CEO 14 Our survey of 652 CFOs around the world suggests that their relationship Change/plans for change in geographical with the CEO has continued to strengthen since the financial crisis. A footprint of the business 13 majority (64%) of those surveyed say that their collaboration with the CEO Change of CEO 13 has increased, driven primarily by new growth opportunities and changes in strategy (see Chart 1). Shortcomings in financial performance 12 Questions from the board 11 Significant merger or divestiture activity 11 % 0 5 10 15 20 25 30 35 40 Partnering for performance Part 5: the CFO and the chief executive officer 4

Partnering for Performance Part 5 Page 5 Page 7

Partnering for Performance Part 5 Page 5 Page 7