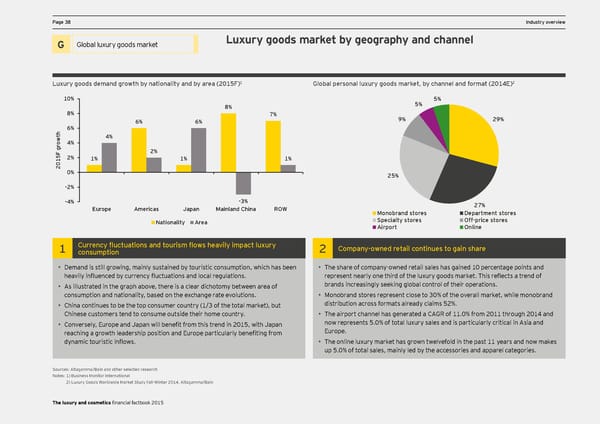

PPage 38age 38 DCF and valuation pIndustry oaramevervieterws Luxury goods market by geography and channel Global luxury goods Title for section G Global luxury goods market H X 1 2 Sales of industry players are expected to grow at a healthy rate, led by double-digit annual growth rate for Luxury goods demand growth by nationality and by area (2015F) Global personal luxury goods market, by channel and format (2014E) Welcome to the third edition of EY’s annual L’Occitane and Natura from FY11A to FY14E. Financial Factbook for the luxury and cosmetics 10% X 5% Increased demand through innovative products will cater to underserved emerging markets. sector. The Factbook combines financial 8% 5% 8% X data, insight from EY’s global team of sector 7% Introduction of eco-friendly, sustainable and naturally derived beauty products and cosmetics will stimulate 6% 6% 9% 29% specialists and opinions of external experts. demand in established geographies. h 6% t 4% w o 4% r Titles for charts g 2% F 5 2% 1% 1% 1% 1 0 2 0% 25% -2% -4% -3% 27% Europe Americas Japan Mainland China ROW Monobrand stores Department stores Nationality Area Specialty stores Off-price stores Airport Online 1 Currency fluctuations and tourism flows heavily impact luxury 2 Company-owned retail continues to gain share consumption • Demand is still growing, mainly sustained by touristic consumption, which has been • The share of company-owned retail sales has gained 10 percentage points and Titles for charts heavily influenced by currency fluctuations and local regulations. represent nearly one third of the luxury goods market. This reflects a trend of • As illustrated in the graph above, there is a clear dichotomy between area of brands increasingly seeking global control of their operations. consumption and nationality, based on the exchange rate evolutions. • Monobrand stores represent close to 30% of the overall market, while monobrand • China continues to be the top consumer country (1/3 of the total market), but distribution across formats already claims 52%. Chinese customers tend to consume outside their home country. • The airport channel has generated a CAGR of 11.0% from 2011 through 2014 and • Conversely, Europe and Japan will benefit from this trend in 2015, with Japan now represents 5.0% of total luxury sales and is particularly critical in Asia and reaching a growth leadership position and Europe particularly benefiting from Europe. dynamic touristic inflows. • The online luxury market has grown twelvefold in the past 11 years and now makes up 5.0% of total sales, mainly led by the accessories and apparel categories. Source: Data based on consensus of several brokers’ reports for each company. Sources: Altagamma/Bain and other selected research NNootteess:: 1Ma) Brkuest cinaepss Mitalioznaittioor In ins bteransaetd oionn a oal ne-month average as of December 2012. T he 20122 g) Lurxouwrty Gh cooorrdes Wspoonrdlds two tide Mhe saraklees gt Srtuodwy Fth raall-tWe binettewr 2ee0n F14Y, A11ltA aaganmd FmYa1/B2aAi/nE. The luxury and cosmetics financial factbook 2015

Seeking sustainable growth - The luxury and cosmetics financial factbook Page 39 Page 41

Seeking sustainable growth - The luxury and cosmetics financial factbook Page 39 Page 41