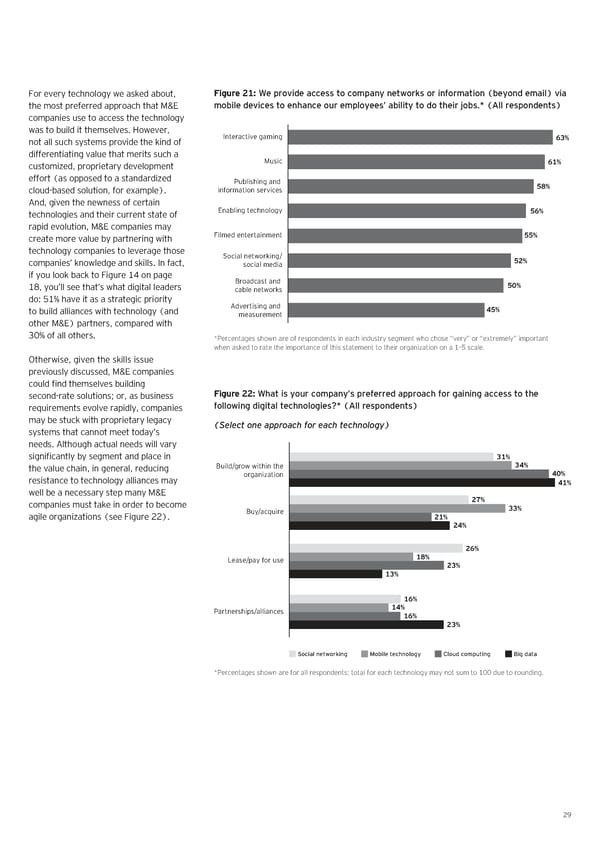

For every technology ‚e asŒed about€ Figure 21: „e proide access to company netor‚s or information ¤beyond email¥ ia the most preerred approach that M&E mobile deices to enhance our employees’ ability to do their «obsˆ¦ ¤ƒll respondents¥ companies use to access the technology ‚as to build it themselvesŠ ‘o‚ever€ Interactive gaming not all such systems provide the Œind o 63% dierentiating value that merits such a customiœed€ proprietary development Music 61% eort ˜as opposed to a standardiœed Publishing and cloudbased solution€ or eamplešŠ information services 58% And€ given the ne‚ness o certain technologies and their current state o Enabling technology 56% rapid evolution€ M&E companies may create more value by partnering ‚ith Filmed entertainment 55% technology companies to leverage those Social networking/ companies’ Œno‚ledge and sŒillsŠ In act€ social media 52% i you looŒ bacŒ to Figure ˆ¥ on page Broadcast and ˆž€ you’ll see that’s ‚hat digital leaders cable networks 50% do’ „ˆ” have it as a strategic priority to build alliances ‚ith technology ˜and Advertising and 45% measurement other M&Eš partners€ compared ‚ith ‰…” o all othersŠ All respondents ¡£ercentages sho‚n are o respondents in each industry segment ‚ho chose “very” or “etremely” important ‚hen asŒed to rate the importance o this statement to their organiœation on a ˆ–„ scaleŠ ƒther‚ise€ given the sŒills issue previously discussed€ M&E companies could find themselves building secondrate solutions• or€ as business Figure 22: „hat is your company’s preferred approach for gaining access to the reuirements evolve rapidly€ companies folloing digital technologies…¦ ¤ƒll respondents¥ may be stucŒ ‚ith proprietary legacy (Select one approach or each technology) systems that cannot meet today’s needsŠ Although actual needs ‚ill vary significantly by segment and place in 31% Build/grow within the 31% 34% Build/grow within the 34% 40% the value chain€ in general€ reducing organization 40% resistance to technology alliances may organization 41% 41% ‚ell be a necessary step many M&E 27% companies must taŒe in order to become Buy/acquire 27% 33% Buy/acquire 21% 33% agile organiœations ˜see Figure ‡‡šŠ 21% 24% 24% 26% Lease/pay for use 18% 26% Lease/pay for use 18% 23% 13% 23% 13% 16% 16% Partnerships/alliances 14% 14% Partnerships/alliances 16% 16% 23% 23% Social networking Mobile technology Cloud computing Big data Social networking Mobile technology Cloud computing Big data ¡£ercentages sho‚n are or all respondents• total or each technology may not sum to ˆ…… due to roundingŠ ¢

Digital Agility Now Page 28 Page 30

Digital Agility Now Page 28 Page 30