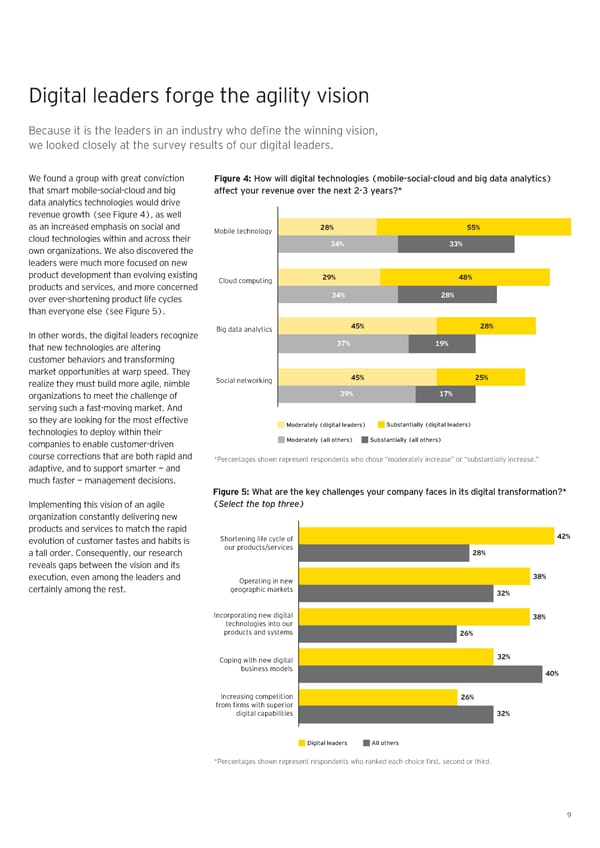

¦igital leaders orge the agility vision ›ecause it is the leaders in an industry ‚ho define the ‚inning vision€ ‚e looŒed closely at the survey results o our digital leadersŠ Že ound a group ‚ith great conviction Figure 4: £o ill digital technologies ¤mobilesocialcloud and big data analytics¥ that smart mobilesocialcloud and big affect your reenue oer the ne‡t years…¦ data analytics technologies ‚ould drive revenue gro‚th ˜see Figure ¥š€ as ‚ell as an increased emphasis on social and Mobile technology 28% 55% cloud technologies ‚ithin and across their 34% 33% o‚n organiœationsŠ Že also discovered the leaders ‚ere much more ocused on ne‚ product development than evolving eisting Cloud computing 29% 48% products and services€ and more concerned over evershortening product lie cycles 34% 28% than everyone else ˜see Figure „šŠ Big data analytics 45% 28% In other ‚ords€ the digital leaders recogniœe that ne‚ technologies are altering 37% 19% customer behaviors and transorming marŒet opportunities at ‚arp speedŠ They 45% 25% realiœe they must build more agile€ nimble Social networking organiœations to meet the challenge o 39% 17% serving such a astmoving marŒetŠ And so they are looŒing or the most eective Moderately (digital leaders) Substantially (digital leaders) technologies to deploy ‚ithin their companies to enable customerdriven Moderately (all others) Substantially (all others) course corrections that are both rapid and ¡£ercentages sho‚n represent respondents ‚ho chose “moderately increase” or “substantially increaseŠ” adaptive€ and to support smarter — and much aster — management decisionsŠ Figure ‚: „hat are the ‚ey challenges your company faces in its digital transformation…¦ Implementing this vision o an agile ¤Select the top three) organiœation constantly delivering ne‚ products and services to match the rapid evolution o customer tastes and habits is Shortening life cycle of 42% a tall orderŠ Conseuently€ our research our products/services 28% reveals gaps bet‚een the vision and its eecution€ even among the leaders and Operating in new 38% certainly among the restŠ geographic markets 32% Incorporating new digital 38% technologies into our products and systems 26% Coping with new digital 32% business models 40% Increasing competition 26% from firms with superior digital capabilities 32% Digital leaders All others ¡£ercentages sho‚n represent respondents ‚ho ranŒed each choice first€ second or thirdŠ ¢

Digital Agility Now Page 8 Page 10

Digital Agility Now Page 8 Page 10