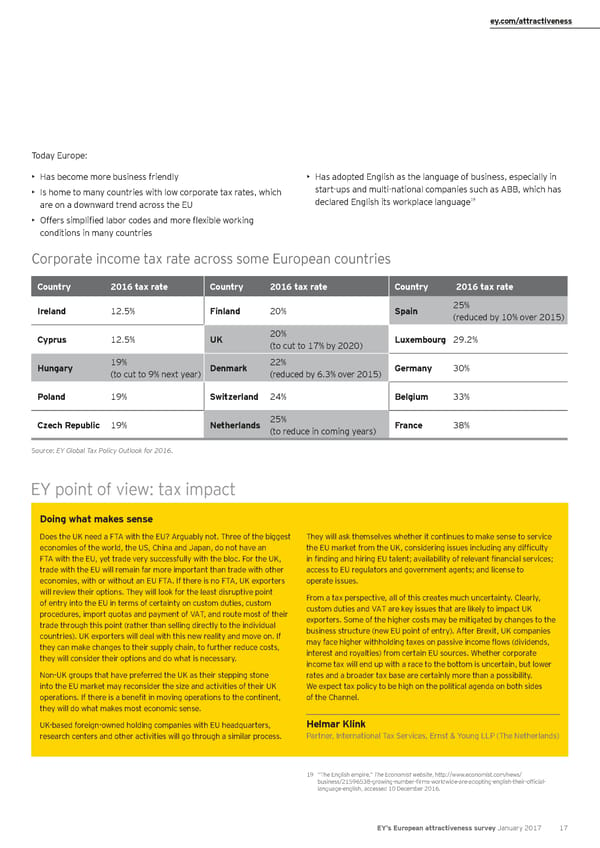

ey.com/attractiveness Today Europe: • Has become more business friendly • Has adopted English as the language of business, especially in • Is home to many countries with low corporate tax rates, which start-ups and multi-national companies such as ABB, which has 19 are on a downward trend across the EU declared English its workplace language • Offers simplified labor codes and more flexible working conditions in many countries Corporate income tax rate across some European countries Country 2016 tax rate Country 2016 tax rate Country 2016 tax rate Ireland 12.5% Finland 20% Spain 25% (reduced by 10% over 2015) Cyprus 12.5% UK 20% Luxembourg 29.2% (to cut to 17% by 2020) Hungary 19% Denmark 22% Germany 30% (to cut to 9% next year) (reduced by 6.3% over 2015) Poland 19% Switzerland 24% Belgium 33% Czech Republic 19% Netherlands 25% France 38% (to reduce in coming years) Source: EY Global Tax Policy Outlook for 2016. EY point of view: tax impact Doing what makes sense Does the UK need a FTA with the EU? Arguably not. Three of the biggest They will ask themselves whether it continues to make sense to service economies of the world, the US, China and Japan, do not have an the EU market from the UK, considering issues including any difficulty FTA with the EU, yet trade very successfully with the bloc. For the UK, in finding and hiring EU talent; availability of relevant financial services; trade with the EU will remain far more important than trade with other access to EU regulators and government agents; and license to economies, with or without an EU FTA. If there is no FTA, UK exporters operate issues. will review their options. They will look for the least disruptive point From a tax perspective, all of this creates much uncertainty. Clearly, of entry into the EU in terms of certainty on custom duties, custom custom duties and VAT are key issues that are likely to impact UK procedures, import quotas and payment of VAT, and route most of their exporters. Some of the higher costs may be mitigated by changes to the trade through this point (rather than selling directly to the individual business structure (new EU point of entry). After Brexit, UK companies countries). UK exporters will deal with this new reality and move on. If may face higher withholding taxes on passive income flows (dividends, they can make changes to their supply chain, to further reduce costs, interest and royalties) from certain EU sources. Whether corporate they will consider their options and do what is necessary. income tax will end up with a race to the bottom is uncertain, but lower Non-UK groups that have preferred the UK as their stepping stone rates and a broader tax base are certainly more than a possibility. into the EU market may reconsider the size and activities of their UK We expect tax policy to be high on the political agenda on both sides operations. If there is a benefit in moving operations to the continent, of the Channel. they will do what makes most economic sense. UK-based foreign-owned holding companies with EU headquarters, Helmar Klink research centers and other activities will go through a similar process. Partner, International Tax Services, Ernst & Young LLP (The Netherlands) 19 “The English empire,” The Economist website, http://www.economist.com/news/ business/21596538-growing-number-firms-worldwide-are-adopting-english-their-official- language-english, accessed 10 December 2016. EY’s European attractiveness survey January 2017 17

European attractiveness survey January 2017 Page 21 Page 23

European attractiveness survey January 2017 Page 21 Page 23